The moment you receive extra income—a significant bonus, a substantial raise, a large tax refund, or the profits from a successful side hustle—it feels like pure financial freedom. Yet, for many people, this sudden influx of cash often vanishes without a trace, spent on impulse buys or absorbed by minor lifestyle upgrades that fail to deliver lasting value.

Managing your regular budget is one challenge; managing discretionary or “extra” funds requires a different, more disciplined approach. This is where the venerable 50/30/20 Rule shines. While typically used for standard monthly budgeting, applying this framework specifically to lump sums of extra income transforms it from a basic spending guide into a powerful engine for accelerated wealth building and debt elimination.

This comprehensive guide will detail how to adapt the 50/30/20 rule to maximize the impact of every dollar of extra income, ensuring that temporary windfalls translate into permanent financial security.

The 50/30/20 Rule: How to Manage Your Extra Income Wisely for Maximum Financial Freedom

Understanding the 50/30/20 Rule in Context

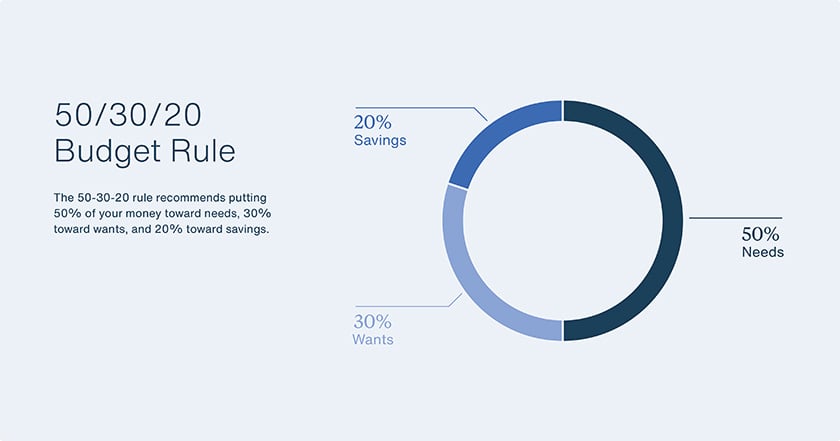

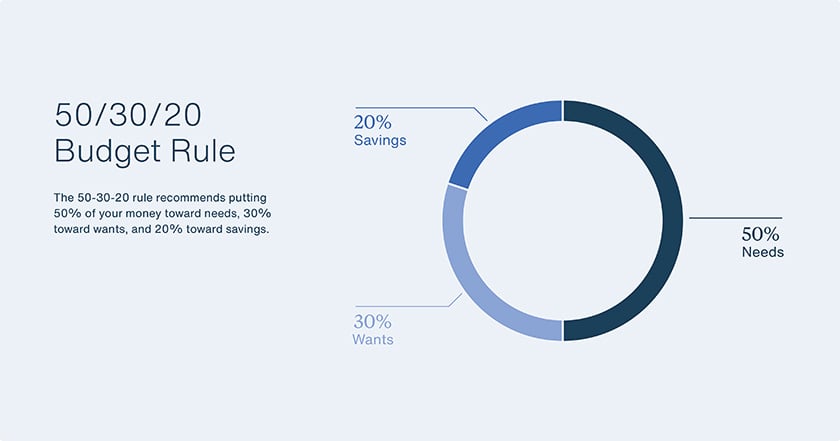

The 50/30/20 rule, popularized by Senator Elizabeth Warren and her daughter Amelia Warren Tyagi in their book All Your Worth: The Ultimate Lifetime Money Plan, provides a simple, structured method for allocating after-tax income. The philosophy is built on three distinct categories:

sumber: www.unfcu.org

- 50% Needs: Essential expenses necessary for survival (housing, utilities, groceries, transportation, minimum debt payments).

- 30% Wants: Non-essential expenses that improve quality of life (dining out, entertainment, hobbies, premium subscriptions).

- 20% Savings & Debt Repayment: Future-focused allocations (retirement contributions, emergency fund, accelerated debt payments).

When dealing with your regular monthly paycheck, the goal is compliance—making sure your necessary expenses don’t exceed 50%. However, when dealing with extra income, the application shifts entirely. The goal is no longer compliance; it is hyper-efficient allocation.

The Critical Difference: Standard Budget vs. Extra Income

If you receive a $10,000 bonus, you do not need to spend $5,000 of it on immediate needs, as your existing paycheck should already cover those. Applying 50/30/20 to extra income means treating the bonus itself as the “income” and allocating percentages based on its potential to accelerate your goals.

In this context, the 50% allocation often becomes focused on future needs or bolstering your existing safety net, while the 20% portion (the growth engine) often receives the most scrutiny and leverage.

The Core Strategy: Applying 50/30/20 to Windfalls and Raises

The first step in managing extra income is acknowledging that it is a strategic asset, not permission to splurge. Whether it’s a $500 bonus or a $50,000 inheritance, the framework remains the same.

Defining “Extra Income”

For the purpose of this rule, “Extra Income” includes any money received beyond your standard, expected monthly budget allocation. This typically includes:

- Annual or quarterly bonuses.

- Tax refunds.

- Raises (the difference between your old and new paychecks).

- Inheritances or gifts.

- Profits from selling assets or side business revenue.

Step 1: The 50% Pillar – Accelerated Needs and Buffer Building

When applying 50% of a bonus or windfall, we focus on accelerating necessary financial stability and tackling large, infrequent needs.

A. Pre-Paying Essential Future Expenses

Instead of using the 50% for immediate needs (which are already covered), use it to pre-pay bills or fund known future expenditures. This creates massive breathing room in your standard monthly budget for the coming months.

- Housing: Pre-pay an extra month or two of rent or mortgage principal.

- Insurance: Pay your six-month auto insurance premium in full instead of monthly installments (often securing a discount).

- Taxes: If you are self-employed, allocate 50% toward estimated quarterly tax payments.

- Vehicle Maintenance: Fund a dedicated maintenance account for upcoming repairs or new tires—a necessary expense that often acts as a financial emergency when neglected.

B. Eliminating High-Interest Consumer Debt (The Priority Need)

While the 20% category is designated for debt repayment, high-interest consumer debt (credit cards, predatory loans) acts as a persistent financial drain—a “negative need.” Many financial experts recommend allocating a significant portion of the 50% category here, especially if your interest rates exceed 10%.

Expert Insight: Paying off debt with a 20% APR is a guaranteed, tax-free 20% return on your money. This is often the highest-value allocation for individuals with substantial balances.

Step 2: The 30% Pillar – Strategic Wants and Quality of Life Investment

The 30% allocation is crucial for preventing “financial burnout.” If you allocate 100% of extra income to debt and savings, you diminish the psychological reward of hard work, making it harder to stay disciplined. The 30% allows for strategic enjoyment.

A. Investing in Efficiency and Future Earnings

Instead of pure consumption, use this 30% to buy things that reduce friction in your life or improve your earning potential:

- Tools for Side Hustles: Upgrading equipment necessary for your secondary income stream (e.g., better computer, professional camera).

- Education: Paying for a certification, course, or conference that directly leads to a promotion or higher salary.

- Quality of Life Upgrades: Purchasing a high-quality item that replaces a cheaper, constantly failing alternative (e.g., a reliable appliance, ergonomic office chair).

B. Intentional Splurging

This is your permission to celebrate. If your bonus is $10,000, $3,000 is available for wants. This is the budget for a memorable trip, a significant piece of furniture, or a meaningful gift. The key is intentionality. By allocating this money upfront, you eliminate the guilt that often accompanies large discretionary purchases.

Step 3: The 20% Pillar – The Engine of Growth and Security

This 20% is the non-negotiable core of future wealth. It must be allocated towards assets that grow or liabilities that are eliminated permanently. When managing extra income, the 20% often becomes the most powerful lever for long-term change.

A. Funding the Emergency Reserve

If you have not yet reached your goal of 3 to 6 months of living expenses saved in an accessible, high-yield savings account, the 20% (or more, if the 50% wasn’t needed for high debt) must be directed here. An extra income buffer is the single most important defense against future financial setbacks.

B. Maximizing Tax-Advantaged Accounts

This is the prime destination for the 20%. Extra income provides the perfect opportunity to “max out” annual contribution limits:

- 401(k) / 403(b): If your employer offers a match, ensure you contribute enough to capture 100% of it. Extra income allows you to front-load these contributions early in the year.

- Roth IRA / Traditional IRA: These accounts offer tax-free growth (Roth) or upfront tax deductions (Traditional). Funding these limits immediately leverages the power of compound interest for the entire year.

- Health Savings Account (HSA): If eligible, the HSA is a triple tax-advantaged powerhouse (contributions are tax-deductible, growth is tax-free, and withdrawals for qualified medical expenses are tax-free).

Advanced Allocation: Optimizing the 20% Growth Engine

For individuals who already have a robust emergency fund and minimal high-interest debt, the management of extra income moves into sophisticated optimization. Here, we focus on the relationship between debt interest rates and potential investment returns.

The Debt vs. Investment Dilemma

A common question is: Should I pay off my mortgage or student loans, or should I invest in the stock market?

The decision hinges on the interest rate of the debt versus your expected investment return. A standard financial planning benchmark suggests:

- If Debt Interest Rate > 6%: Prioritize paying down the debt aggressively. The guaranteed return from eliminating a 7% student loan is often safer and more reliable than market returns.

- If Debt Interest Rate < 4%: Prioritize investing, especially in tax-advantaged accounts. It is highly probable that the market will return more than 4% over the long term, making the leverage worthwhile.

- If Debt Interest Rate is 4%–6%: This is a gray area. A balanced approach is often best—split the 20% between investment and accelerated debt principal payments.

Unique Insight: The Psychological Win. Even if the math slightly favors investing, eliminating a debt entirely (like a car loan or student loan) provides an enormous psychological boost, freeing up monthly cash flow that can then be permanently redirected toward investment. This monthly cash flow increase is often worth more than a marginal difference in returns.

The Power of the “Reverse 50/30/20” for High Earners

The standard 50/30/20 rule is designed primarily for those balancing needs and desires. For high-income earners whose needs are easily met by less than 50% of their income (or whose extra income is very large), a “Reverse 50/30/20” approach can be more effective.

In this model, the goal is to shift priorities dramatically toward wealth accumulation:

- 50% Savings & Investment: Aggressively funding retirement, brokerage accounts, and real estate goals.

- 30% Needs: Covering all essential living expenses.

- 20% Wants: Allowing for discretionary spending and lifestyle upgrades.

When high earners receive a bonus, they should treat 100% of that bonus as the new income stream and immediately apply the 50% investment allocation, using the remaining 50% for high-value wants or accelerated debt elimination.

Building the “Freedom Fund”

Extra income provides the ideal fuel for a “Freedom Fund”—money specifically earmarked for achieving a major long-term goal that grants significant personal freedom, such as:

- The down payment for a first rental property.

- The capital necessary to launch a business.

- Funding a sabbatical or career pivot.

By dedicating a portion of the 20% to this specific, motivating goal, you turn abstract savings into concrete, achievable dreams.

Troubleshooting and Flexibility: Adapting the Rule to Your Life Stage

The 50/30/20 framework is a guideline, not a rigid law. The greatest strength of this methodology, particularly when applied to extra income, is its adaptability based on your current financial life stage.

When to Aggressively Shift Allocations

Your life circumstances dictate which pillar needs the most support. When extra income arrives, you must assess your current financial weak points:

A. High Debt Phase (Ages 20–35)

If you are burdened by high student loans or credit card debt, the rule should temporarily become 70/10/20 (70% to debt/savings, 10% wants, 20% needs buffer), or even 80/10/10 for the extra income. The immediate priority is eliminating the drag of high interest before prioritizing investment.

B. Family Expansion Phase (Ages 30–45)

Extra income during this phase should heavily fund future needs. The 50% allocation should prioritize building a robust college savings plan (529 accounts) or increasing term life insurance coverage, which are crucial future needs often neglected in standard budgeting.

C. Pre-Retirement Phase (Ages 50+)

If retirement is less than 15 years away, the 20% allocation must be maximized to take advantage of “catch-up contributions” available in 401(k)s and IRAs. Extra income should be directed almost entirely toward tax-advantaged retirement vehicles, possibly shifting to 10/10/80 (10% needs buffer, 10% wants, 80% savings/retirement) for lump sums.

The Behavioral Finance Component: Defeating Lifestyle Creep

The most significant threat to extra income is “lifestyle creep”—the insidious tendency for spending to rise commensurate with income, leaving you no better off financially. The 50/30/20 rule is the perfect antidote.

By structuring the allocation immediately upon receipt, you automate discipline. When you receive a raise, for instance, you should:

- Calculate the exact monthly increase (the “extra income”).

- Immediately automate 20% of that increase to a brokerage or retirement account.

- Automate 50% of that increase toward accelerated debt or savings goals.

- Only allow the remaining 30% to flow into your discretionary “wants” budget.

This proactive approach ensures that the majority of your increased earning power is secured for your future, while still allowing for a sustainable, guilt-free improvement in your current life quality.

Conclusion: The Path to Permanent Prosperity

The 50/30/20 rule is more than a budgeting tool; it is a framework for intentionality. When applied to extra income, it ensures that every bonus, raise, or windfall serves a deliberate purpose—whether that is immediate debt relief, bolstering future security, or investing in meaningful life experiences.

The wealth accumulated by financially savvy individuals is rarely the result of one massive score; it is the cumulative effect of consistently wise decisions regarding marginal income. By adopting this structured approach, you move beyond simply spending your extra money and begin leveraging it, transforming temporary gains into permanent, enduring financial freedom.

Start today. Define your “extra income,” apply the percentages, and watch how quickly your financial trajectory shifts.

sumber : Youtube.com